Apple stock isn’t the value investment it used to be.

Warren Buffett and Berkshire Hathaway are among the most famous Apple (AAPL 0.50%) investors. They started their position in 2016, continually added to it, and rode Apple’s growth to impressive gains. However, they’ve been dumping Apple shares steadily each quarter in 2024. Is it time for other investors to follow suit? After all, the stock is trading near all-time highs.

Buffett’s move is not what it seems

Berkshire’s Apple stake was biggest in in the third quarter of 2023 at around 915 million shares, making up 50% of its overall portfolio. That’s a massive concentration, more than many investors would have chosen.

However, that’s not why Buffett decided to sell it. Because Berkshire added to its Apple position along the way, it is sitting on massive gains. Massive gains mean a large tax bill when it comes time to sell. Currently, the capital gains tax rate sits at 21%, a historically low figure. However, there are many proposals to increase this rate to 28%, which would increase the amount of taxes Berkshire owes on its Apple gains.

This is the primary reason Buffett is dumping Apple stock: He wants to realize as much of a gain as possible by capitalizing on the low tax rate. He also stated that Apple will likely remain one of Berkshire’s largest positions.

After peaking at 915 million Apple shares in Q3, Berkshire reduced its stake to 905 million in Q4, 789 million in the first quarter of 2024, and 400 million in Q2. That’s a rapid drawdown, and investors will be curious to see what Berkshire and Buffett have done in the third quarter of this year. That information will be available 45 days after the close of Q3, so investors will get to see Buffett’s moves on November 15.

I predict more Apple stock will be sold by Berkshire, as part of the investment thesis has disappeared.

Apple isn’t what it used to be

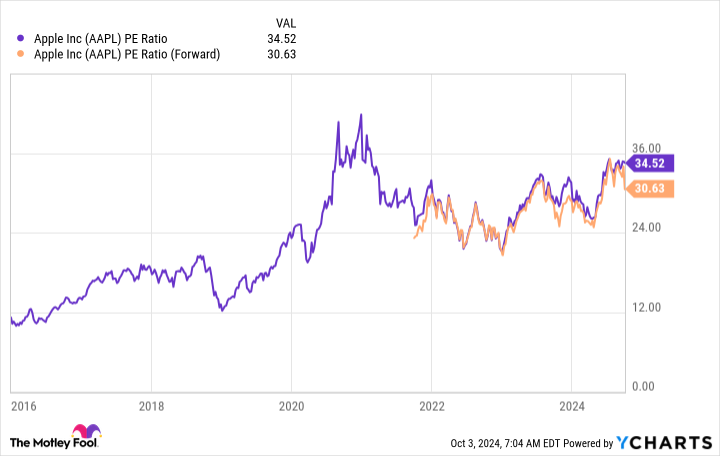

When Berkshire first took a position in 2016, Apple was trading for around 11 times earnings — a classic Buffett value investment. Now that value no longer exists.

AAPL PE Ratio data by YCharts

Apple now trades at an expensive 34.5 times trailing earnings and 30.6 times forward earnings. This could be overlooked if Apple were introducing innovative new devices, selling iPhones like never before, or leading in artificial intelligence. But it’s doing none of that, and its growth suffered.

Since the start of 2023, Apple’s best quarter of revenue growth has delivered a paltry 4.9% sales growth. That’s not indicative of a company that should trade at 34.5 times earnings.

Buffett is a value investor who likes a margin of safety in his investments. There is absolutely no margin of safety in Apple right now, as it’s trading at a premium price without growing much.

While Buffett may be saying Berkshire is selling Apple stock for tax purposes, I think there’s more to the story. If Buffett came out and said, “Apple stock is overvalued, so I’m selling,” that would cause a panic, and investors would dump the stock overnight. Berkshire’s position is massive, and selling it off will take a long time, so Buffett is likely playing the long game.

Apple’s stock is valued too highly for its performance, and I think investors should follow Buffett’s lead and exit the stock before it trades at a more reasonable price tag. The broader market (as measured by the S&P 500 index) trades at 24.2 times trailing earnings, and if Apple reverted to a similar price tag, the stock price would fall by about 30%.

Plenty of companies are cheaper and have better growth than Apple, and investors would be better suited owning those.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple and Berkshire Hathaway. The Motley Fool has a disclosure policy.

{kind=link}